Watch Auction Market 2021 Revisited

• Highest total sales of the Big Four ever

• Highest year by year growth of the total sales

• Highest average sales per lot sold ever

• Highest ever sale event in the history of watch auctions

• Highest only sales ever in the history of watch auctions

• Highest number of seven-figure lots ever sold in watch auctions

• Countless world records

In 2021, the total sales climbed from roughly USD 347mil (2020) to USD 608mil (and if we include charity lots, USD 645mil!), a year-on-year growth of 75% (86%). There hasn’t been any year in the past two decades when the Big Four have delivered a larger growth of their total sales on a year-by-year basis. One might guess that this was because 2020 was a bad year, largely due to Covid. It was not. As you can see from the following chart, 2020 was, in the end, a very successful year given the circumstances ending only about USD 2.6mil below 2019 which is a statistical decline of less than 1%. The year 2021 was remarkable and maneuvered the watch (auction) market into a new dimension. Congratulations to all auction houses. We had fun participating in these events!

So, what made the year 2021 so special?

The answer isn’t easy because in a complex environment, certain factors must work together to attain such incredible results. We have, therefore, picked some key watch growth drivers (leaving aside economic factors):

Soaring number of high value lots sold

Obviously, these points to a significant number of 7-figure lots that were sold. In the past, a million dollar lot was a talking point; in 2021, it became almost “the norm”.

Million Dollar lots in 2021 include 27 sold by Phillips. In 2020? 15 watches. And the year before that? 12 watches. In a span of two years, million-dollar and multi-million-dollar watch sales at a single auction house have more than doubled.

Let’s look at it from a league table point of view. In 2020, only one watch entered the top 10 of the most expensive watches ever sold, which was the Worldtimer Guilloché reference 2523/1 sold by Phillips in Geneva. The year before, beside the charity Only Watch Patek Phillip Grandmaster Chime Ref. 6300A-010, only the Gobbi “Heures Universelles” Ref. 2523 and the Daytona Unicorn Ref. 6265 entered the seven-figure club. So, all together four pieces in four years before 2021. In the past it was rare to see such high numbers. But in 2021, four watches entered the top ten list:

1. Patek Philippe, Ref. 27001M-001

Patek Philippe Complicated desk clock - Ref. 27001M-001 for Only Watch 2021 (Image: Christie’s)

2. Patek Philippe, Ref. 1518 Pink on Pink

Patek Phillipe, Perpetual Calendar Chronograph Ref. 1518 in 18K rose gold originally owned by the Prince Tewfik Adil “T.A.” Toussoun of Egypt (Image: Sotheby’s)

3. Patek Philippe, Ref. 2523

Patek Phillipe, Two-Crown World Time, Ref. 2523 with “Eurasia / Silk Road” cloisonné enamel dial (Image: Phillips)

4. Patek Philippe, Ref. 5711/1A-018

Patek Phillipe, Nautilus, Ref. 5711/1A-018 celebrates the 170-year alliance between Patek Philippe and Tiffany & Co with “Tiffany Blue” lacquer dial sold for the benefit of The Nature Conservancy

Increased average value per lot at live auctions

A key performance indicator for any auction house is the average value per lot sold. The year 2021 was also a success because auction houses managed to increase the average value per lot. Surely this is influenced by the market environment and number of high value lots and less by the commission scheme, which didn’t change much in 2021 compared to the year before.

Soaring demand for recent or in-production watches

There is soaring demand for recent and in-production watches as well as long waiting times at authorized dealers (ADs). Put in context, the share of near or in-production watches was in 2020 fewer than half the number sold in 2021.

Critics would say that these figures show that part of the growth was driven by speculators rather than collectors and I tend to agree with that; “Easy money” leveraging stock markets or crypto trade gets quickly transferred into luxury assets like watches. But I would argue that this can’t be the sole reason. Even established collectors can’t get watches at their AD and at ever increasing prices, some might fall into a “trap” and end up with a brand-new Daytona or Royal Oak at an auction as an investment.

Rolex, GMT-Master II Ref. 126715CHNR originally sold in June 2021 before going under the hammer again in November 2021 (image: Phillips)

Patek Philippe, Ref. 5711/1A – 014 with “green dial” which was sold just a few weeks before being auctioned at Antiquorum in July 2021 (Image: Antiquorum)

“Independents” are in demand and more established at auctions

Most relevant independent watch brands have recent production pieces. Also, they mostly produce limited pieces. What we have seen in 2021 is a continuation of the 2019 and 2020 trend where demand for timepieces from manufacturers such as Philippe Dufour, F.P. Journe and Richard Mille is increasing. Watches sold are setting new world records in most cases; several times above their original retail prices and surpassing the typical auction stars of the past. The Philippe Dufour Grande et Petite Sonnerie #1 at Phillps in Geneva, for example, sold for USD 5,182,109, which was a world record for a Philippe Dufour watch at an auction and a watch by any independent watchmaker ever. But wait, didn’t a similar watch sell for significantly more elsewhere? We will go into that later.

Philippe Dufour, Grande & Petite Sonnerie, N°1 in yellow gold sold at Phillips in Geneva in November 2021 (Image: Phillips)

In 2021 vintage watches might not look like a competitive investment compared to recent or in-production watches. Looking at it from a longer term perspective, however, they have little volatility and as they attract collectors rather than speculators, they have a (very) “long” market and are assets that tend not to be sold. The sheer rarity of them makes them a “safe haven” compared to, say, a standard Rolex Submariner “Hulk” Ref. 116610LV that sold for a stunning USD 94,500 (over four times the trading price on large online trading platforms) at the Phillips New York sale.

Rolex, Submariner, Ref. 116610LV sold at Phillips in NY in December 2021 (Image: Phillips)

Rolex Datejust "Ovettone" Ref. 6105 new old stock condition sold at Monaco Legend Group in October 2021

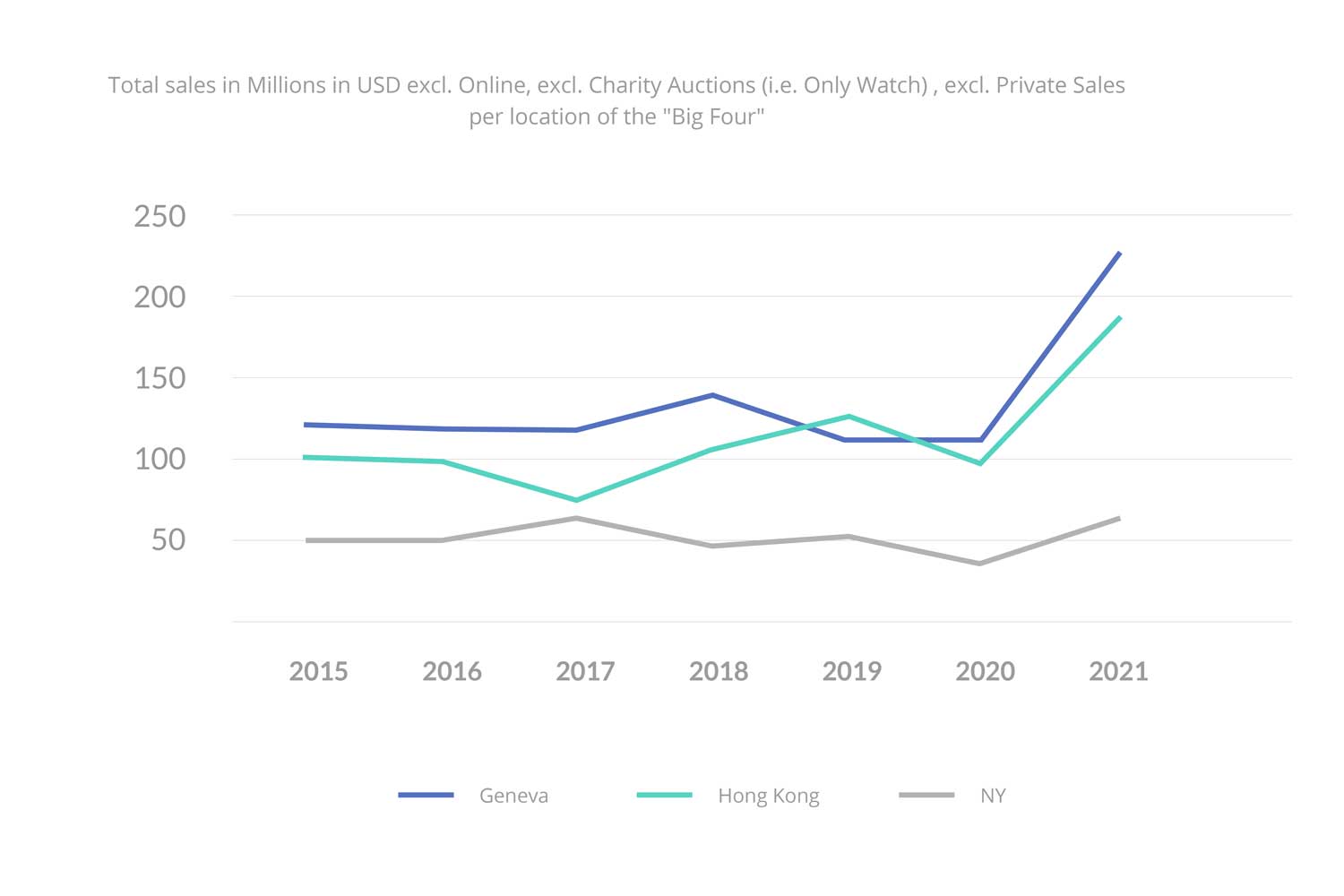

Geneva and Hong Kong battle for #1 auction location

In terms of location, Geneva is still the epicenter of live watch auctions but the battle between Geneva and Hong Kong is intensifying.

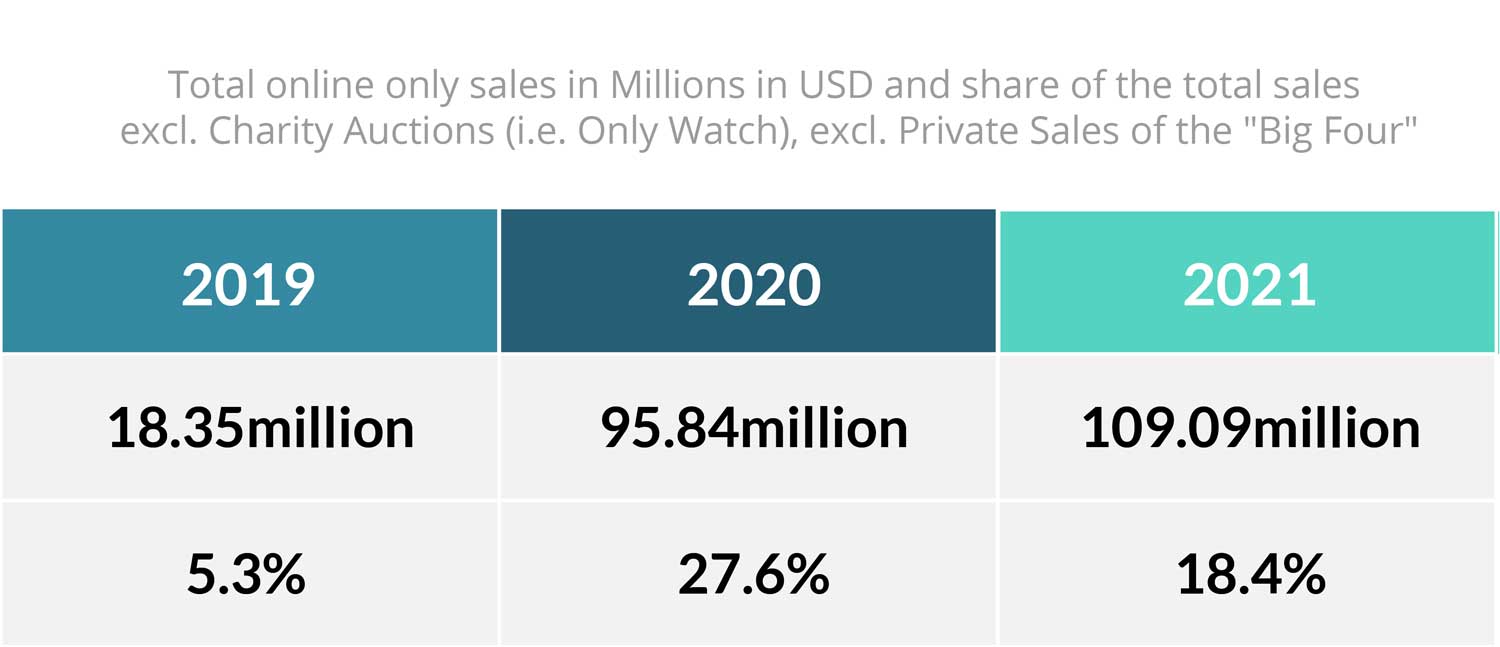

Share of online-only increases and auction houses diversify into the retail market

Besides the extremely high number of online bidders at live auctions – Phillips, for example, announced that 92% of lots offered in their sales received online bids, and 58% of lots sold went to online bidders – online-only sales drive the auction market. Back in 2020, we saw a shift of sales towards online-only; Sotheby’s was the leader with weekly sales generating 48% of the total share of online-only sales among the Big Four. The year 2021 has seen an overall increase of online-only sales: Christie’s now holds 69% of the market of online-only sales of the Big Four. The overall share of the total online-only sales decreased but the absolute amount increased by 14% year on year:

Not all auction houses publish detailed data as Phillips does, but we can assume that the percentage of the sold lots that went to online bidders in live and online auctions is about 60-70% of total sales.

So, are we looking at a bright future or a cooling watch auction market?

If you read what most auction houses predicted for 2021, you’ll realise that they are mostly wrong. Why? Because there are many factors not within their control. Some of the key questions for 2022 and beyond that have yet to be answered include:

• Will we see cooling prices of recent and in-production watches? As growth is in the secondary market at the moment, we might witness a correction of prices. Most buyers are “non-classic” collectors and tend to sell more quickly because they are less emotionally attached to their timepieces. If the premium for recent and in-production watches goes down and consigners realise that auction houses are generating more upside than they are – at literally no risk – they will refrain from consigning and buying these pieces at auctions. If prices of recent and in-production pieces stay high or continue to go up, we will see a further increase of total sales in 2022. If prices of such pieces come under pressure, auction houses will have to do more to find stellar vintage pieces. It will be interesting to see if auction houses are able to tempt back traditional collectors of modern and vintage timepieces to consign their watches after focusing mainly on new clients in 2021 and surfing the modern market wave.

• Will online auction sales be the main growth driver in 2022? My answer is yes, especially for recent and in-production watches which tend to have a higher share of auction lots sold. It’s cost efficient for auction houses and comfortable for buyers, as well as consigners (more frequent and less dependent on time and venue), not forgetting that Covid will also be a factor in 2022. But there’s a disadvantage of online-only auctions compared to live auctions: They are missing the “live factor”, including the thrill that sometimes happens during live auctions. Online-only auctions usually take place over one or two weeks and bidders (especially non-professional) get quickly distracted. Hence to be able to sell higher value pieces successfully at online-only auctions, the live factor should be incorporated. We will most likely see online-only single-day events in 2022.

• Will the Big Four be able to source watches? At the end, the success of auction houses depends significantly on the quality and quantity of watches consigned to them. If you compare the net auction results to prices generated outside of auctions, you can see how they compete long term, especially at buyers’ commissions of 25% and above or total fees to the seller (and buyer) of about 30%.Twenty years ago, the Big Four had a 15% buyer’s premium. In 2021 the buyer’s premium is between 25% and 26%. Whilst 20 years of inflation might have an impact on prices, one wonders why the commission rate of online auctions, with little to less effort, compared to a live auction (no printed catalogue, no preview tours, etc), isn’t significantly lower. Also, “challenger” auction houses, such as the growing Monaco Legend Group, have their own strategies. Monaco Legend Group will, no doubt, continue to grow and carve out its own identity and loyal client base who might have traditionally gone with one of the “Big Four”. Another challenger is Loupe This, where the buyer commission is only 10%, making it attractive for buyers to buy and the frequency of auctions makes it appealing to consign.

Let’s look at the Philippe Dufour Grande et Petite Sonnerie #1. A Collected Man announced the sale of Philippe Dufour Grande et Petite Sonnerie Wristwatch for USD 7.63mil around three months before the Phillips auction. If sold at the asking price, this represents at least a 50% higher result for the seller.

• Will the “sales” be closed? “100% lots sold through” is a term we saw again in 2021 for some of the Big Four events. The reality is that unpaid lots and bad debts are growing issues for auction houses; while they have always been of concern, in 2021 the number of pending sales rose to a new level. Most auction houses solve those issues in the best interest of their consignors and pay the hammer price. But what if seven-figure lots aren’t paid? This can significantly impact the cash flow of auction houses. As long as interest rates are close to zero, it might not be an issue to re-finance, but what if that changes?

• Will smaller watch auction houses finally will be relevant? The total sales of other watch-related auction houses is about 20% of the total sales value of Big Four. Most of these “hidden champions” are auction houses that are family-owned and still entrepreneurially driven so their cost base is likely to be lower. They also tend to ask for lower commissions to gain an advantage over the established Big Four. In terms of relevance, they have no other choice than to grow sales to attract consigners going forward. It’s “grow or go” if you have no philanthropic funding. Staying small isn’t the best option if you want to build equity value in the auction business. My assumption is that you must have at least 10% market share of the Big Four sales to be relevant in the market. This is roughly USD 60mil on an annual basis. None of these smaller auction houses come close to this figure, but the chances have never been better as the Big Four tend to leave classic collectors aside and follow market sentiment. More and more we hear that the level of expertise at the Big Four is significantly dropping; it’s no wonder, if the majority of lots are recent or in-production. Younger and less experienced teams may not get to see vintage watches and gain experience and expertise. Selling modern watches is more about allocation and less about having an in-depth understanding of watches. Going forward, this could be challenge for the Big Four while the smaller challengers might have a good chance to grab market share.

As mentioned, the combination of several factors must be present to make an auction year a success. Let’s cross fingers that 2022 will be another blast.

Preliminary data and insight have been taken from the bi-annually published detailed market report of the primary watch auction market from Rare & Fine Vintage Watches. It can be ordered on a subscription basis through marketreport@rareandfine.com

Illustrated figures may differ from published figures of auction houses as they exclude charity sales (if not otherwise mentioned), private treaty as well as curated sales where watches are only part of the sale. Currency conversion might impact total results.

You may also like

News

Jacob & Co. Goes Minimal with the Astronomia Régulateur

Jul 10, 2026

News

Jacob & Co. Goes Minimal with the Astronomia Régulateur

Jul 10, 2026

News

Australia’s Largest Exhibition of Cartier is on in Melbourne, Right Now

Jul 9, 2026

News

Australia’s Largest Exhibition of Cartier is on in Melbourne, Right Now

Jul 9, 2026

News

Bangkok Watch Week Returns For A Bigger Second Edition In 2026

Jul 3, 2026

News

Bangkok Watch Week Returns For A Bigger Second Edition In 2026

Jul 3, 2026